The Case

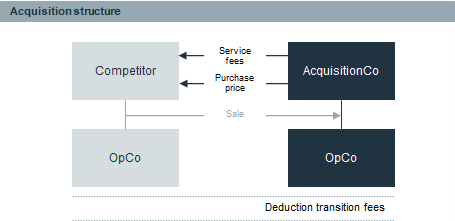

- The client acquired via an acquisition company (‘AcquisitionCo’) part of the activities of a competitor (operated by OpCo), agreeing to pay € 18.4 million post-acquisition service fees on top of the purchase price.

- No similar fees were charged when OpCo resorted under the seller’s umbrella. The tax authorities challenged their deductibility arguing that the service fees should be characterised as (non-deductible) goodwill or earn-out payments. Non-deductibility of the service fees would translate into a significant increase of the effective tax rate on OpCo’s activities.

- Client intended to litigate the case, but had difficulties to generate sufficient evidence for its position that the payments were operational service fees, because all key staff involved in the acquisition had left the firm and client had no access to seller’s information.

The Challenge

The client wanted counsel

- to give an evaluation of the case and the chances of a successful litigation; and

- to set out how it could negotiate a settlement with the authorities.

The Solution

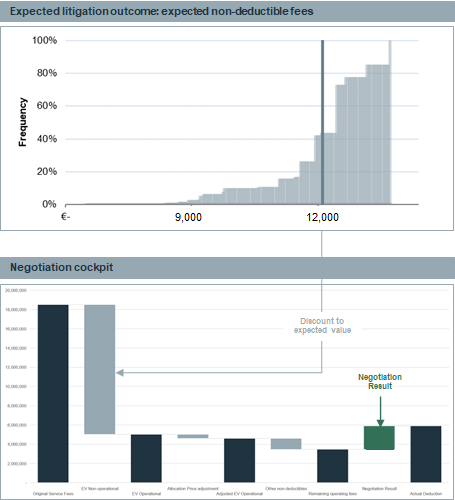

- First, the likelihood of qualification as a deductible operational fee was assessed, accounting for the difficulties to provide supporting evidence and the technical merits of the case.

- It was estimated that, in litigation, client could expect an amount of €4 – €7 million to be deductible.

- To prepare for the settlement negotiations, the most sensitive fee categories were identified, enabling the client to focus on the fees with the highest deduction value.

- Based on the model, management decided that a settlement was preferable over litigation.

- Then a negotiation model was prepared, allowing to translate offers in the negotiation process into financial effects.