The Case

A banking group had net operating losses (‘NOLs’) from its operating companies who were part of a consolidated tax group. The NOLs were recognised as deferred tax asset (‘DTA’) in the commercial accounts.

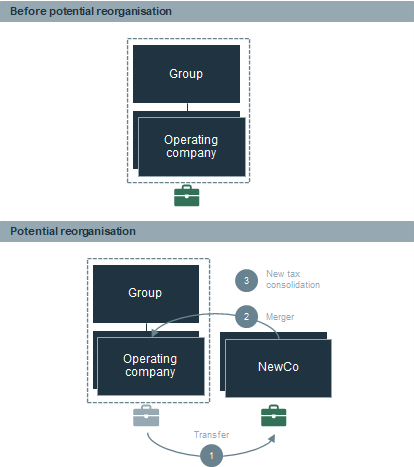

A banking group had net operating losses (‘NOLs’) from its operating companies who were part of a consolidated tax group. The NOLs were recognised as deferred tax asset (‘DTA’) in the commercial accounts.- As the NOLs were to evaporate, the group wished to secure its DTA through a complex corporate reorganisation, through which it would realise taxable gains that could be offset against the NOLs and generate tax base for amortisation. Securing the DTA was important to avoid a drop in the Group’s equity position.

- However, the Group’s board wished to limit the significant operational impact of a potential reorganisation.

- The reorganisation’s DTA-effect was uncertain as the NOL utilisation rules are complex and can have counterintuitive effects, the future income potential of the various operations was uncertain, the valuation of the transferred assets was uncertain, and the amortisation term and residual values of the reorganised assets were unknown.

- Therefore, it became unknown whether securing the DTA would outweigh costs and operational constraints of the reorganisation.

The Challenge

- The Group’s board wished to have insight in the potential trade-offs between the expected positive DTA-effect of a reorganisation and the costs and operational constraints of the reorganisation, given the uncertain economics of the business.

The Solution

The Solution comprised a long-term financial model that enabled tax management to analyse the effect of the reorganisation in which it could include or exclude each operating company (‘OpCos’).

The Solution comprised a long-term financial model that enabled tax management to analyse the effect of the reorganisation in which it could include or exclude each operating company (‘OpCos’).- The model comprised a clear cockpit which allowed management to “play with the numbers” to get a better understanding of the sensitivities of the various value drivers, such as the multiples at which the reorganisation would take place, the effect of amortisation and the fiscal year in which the planning could be carried out without having to understand the technical details of the NOL rules.