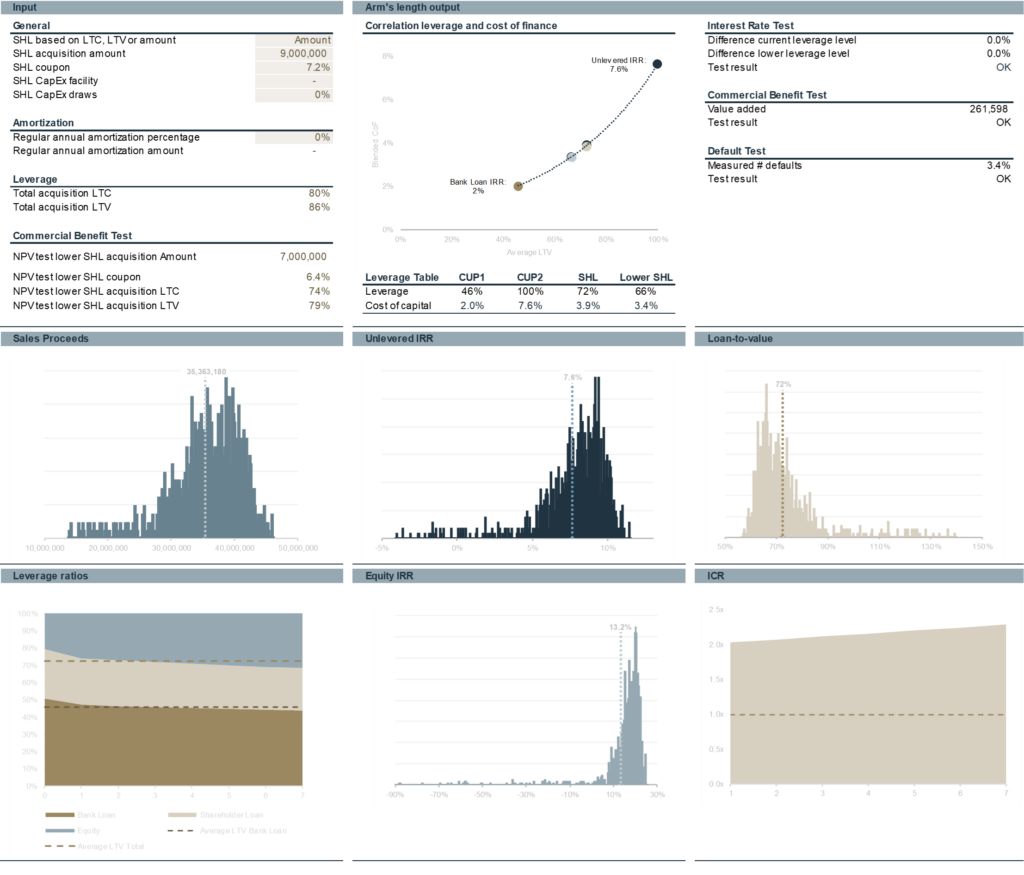

The Case

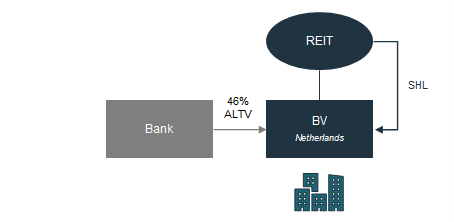

A non-Dutch investor (‘LP‘) with REIT status invested in a Dutch real estate portfolio via a Dutch SPV (‘BV‘).

A non-Dutch investor (‘LP‘) with REIT status invested in a Dutch real estate portfolio via a Dutch SPV (‘BV‘).- 51% of the investment was funded with a 2% third-party bank debt attracted by BV, translating in a 46% average loan-to-value (‘ALTV‘) over the bank loan’s lifetime. The bank interest generated an interest tax shield.

- LP wished to further enhance the tax shield by increasing BV’s leverage with a subordinated “shareholder loan” (‘SHL‘) provided by LP to BV.

- For the interest to be deductible, Dutch law requires that both debt volume and interest must be at arm’s length and the loan may not qualify as a so-called uncommercial loan.

- No reliable benchmark data is available to reasonably establish whether the loan volume and interest rate on a subordinated loan is at arm’s length. In particular, there are comparability constraints because of specific terms and conditions included in the SHL.

The Challenge

Client wished to optimise its interest shield by establishing the SHL’s arm’s length interest rate at a maximum allowed level of leverage (i.e., a level at which the loan would not be qualified as an uncommercial loan).

The Solution

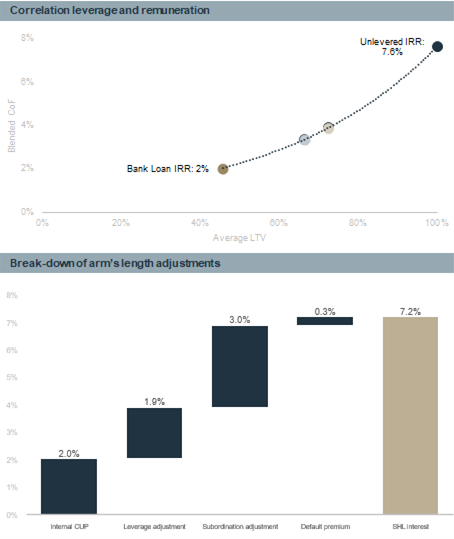

Huygens first established the (exponential) correlation between expected returns and the level of leverage, using the expected return on the bank loan as an internal comparable (‘Internal CUP‘) and using the expected unlevered return on the investment to establish the slope of the exponential correlation, see the upper graph.

Huygens first established the (exponential) correlation between expected returns and the level of leverage, using the expected return on the bank loan as an internal comparable (‘Internal CUP‘) and using the expected unlevered return on the investment to establish the slope of the exponential correlation, see the upper graph.- Using the exponential correlation between expected return and leverage, Huygens secondly established a leverage adjustment to account for the higher level of leverage that results from the SHL top-up.

- Thirdly, a subordination adjustment was made, accounting for the SHL’s subordination to the bank loan and for the specific terms e.g., pay-if-you-can option, CapEx facility, amortisation schemes.

- Fourthly, a default premium was established by performing a Monte Carlo simulation to establish the SHL’s default risk under 2,000 economic scenarios.

- Fifthly, the Monte Carlo simulations were used to stress test the SHL’s debt service capacity under 2,000 economic scenarios and to confirm that a commercially behaving borrower would have a commercial benefit from taking on the SHL at the analysed leverage level.