The Case

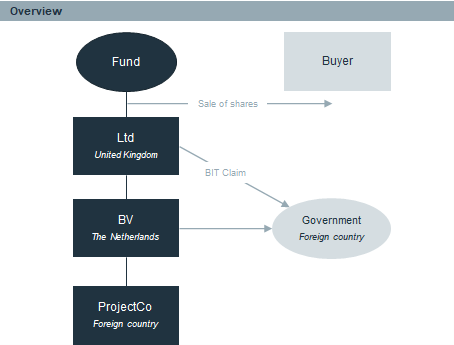

A private equity fund (‘Fund’) held 30% of the shares in an infrastructure project company (‘ProjectCo’) via a Dutch holding (‘BV’) and a UK Holding Ltd. (‘Ltd’).

A private equity fund (‘Fund’) held 30% of the shares in an infrastructure project company (‘ProjectCo’) via a Dutch holding (‘BV’) and a UK Holding Ltd. (‘Ltd’). - The project was awarded a government license, which – after a political change – the new government refused to extend.

- Fund management lodged and won an arbitration procedure under both the Dutch and UK bilateral investment treaties with that third country (‘BIT Claim’).

- Approaching Fund’s closure, Fund Management wished to accelerate the monetisation of the award by divesting the shares in Ltd (and thus indirectly in BV) to a specialised award enforcement funder (‘buyer’).

- In the price negotiations, buyer’s counsel discounted 25% for corporation tax on the award, which Fund’s counsel disputed on the basis of the (tax technical) arguments that

- BV lacked the functionality to be allocated the award;

- the award would be exempt under the participation exemption; and

- at least part of the award should be allocated to Ltd, not BV.

The Challenge

- Fund management and buyer wished to resolve the uncertain tax issue and sought coverage under a W&I insurance policy, the cost of which would be shared between the parties.

- To prepare for price negotiations with the insurance company, fund management and buyer wished to have an estimate and substantiation of the insurance premium.

The Solution

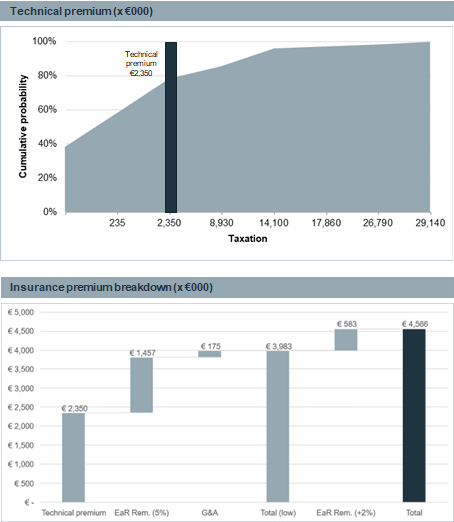

The technical insurance premium was calculated by analysing all possible tax scenarios in a decision table analysis. The technical premium is the probability weighted average of all possible scenarios, which according to the analysis was €2.35 million.

The technical insurance premium was calculated by analysing all possible tax scenarios in a decision table analysis. The technical premium is the probability weighted average of all possible scenarios, which according to the analysis was €2.35 million.- Subsequently, the insurance company’s equity at risk (‘EaR’) was established, being the maximum loss from insurance with a 99.5% confidence level, which was analysed to be €29.14 million. On the EaR the insurance company would seek an estimated 5-7% return, i.e. €1,457,000-€2,040,000.

- It was finally estimated that approximately €175,000 had to be added for general and administrative expenses (‘G&A’).

- The estimated insurance premium would range between €3,983,000 and €4,566,000 exclusive of insurance tax, see breakdown.

- The analysis provided parties with the relevant ingredients to negotiate a premium that was acceptable to both.